Correlation and Simple regression

Correlation

Pearson Correlation

In statistics, the Pearson correlation coefficient, also referred to as the Pearson’s r, Pearson product-moment correlation coefficient (PPMCC) or bivariate correlation, is a measure of the linear correlation between two variables X and Y. It has a value between +1 and −1, where 1 is total positive linear correlation, 0 is no linear correlation, and −1 is total negative linear correlation. It is widely used in the sciences. It was developed by Karl Pearson from a related idea introduced by Francis Galton in the 1880s.

Source: Wikipedia

PMCC

\[r_{xy} = \frac{{COV}_{xy}}{S_xS_y}\]

Where \(S\) is sthe standard deviation and \(COV\) is the covariance.

\[{COV}_{xy} = \frac{\sum_{i=1}^N (x_i - \bar{x})(y_i - \bar{y})}{N-1}\]

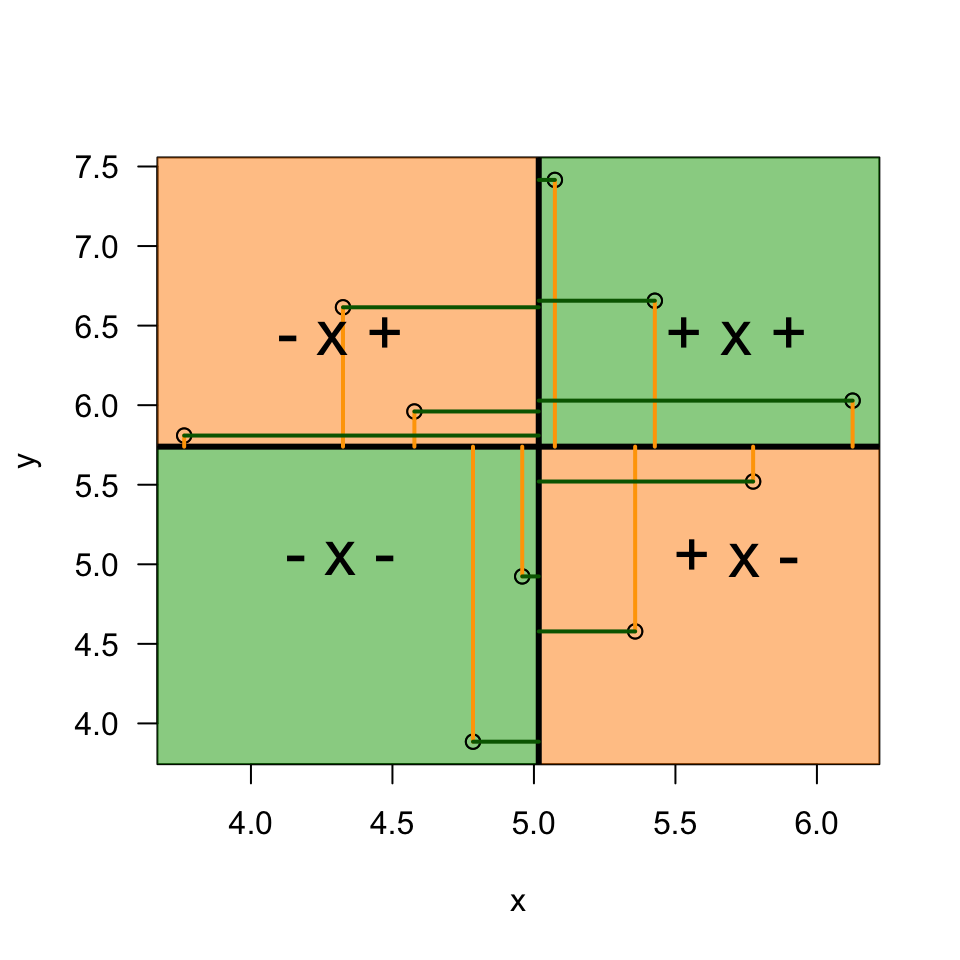

Plot correlation

set.seed(565433)

x = rnorm(10, 5)

y = rnorm(10, 5)

plot(x, y, las = 1)

m.x = mean(x)

m.y = mean(y)

polygon(c(m.x,8,8,m.x),c(m.y,m.y,8,8), col = rgb(0,.64,0,.5))

polygon(c(m.x,0,0,m.x),c(m.y,m.y,0,0), col = rgb(0,.64,0,.5))

polygon(c(m.x,0,0,m.x),c(m.y,m.y,8,8), col = rgb(1,.55,0,.5))

polygon(c(m.x,8,8,m.x),c(m.y,m.y,0,0), col = rgb(1,.55,0,.5))

points(x,y)

abline(h = m.y, lwd = 3)

abline(v = m.x, lwd = 3)

segments(x, m.y, x, y, col = "orange", lwd = 2)

segments(x, y, m.x, y, col = "darkgreen", lwd = 2)

text(m.x+.7, m.y+.7, "+ x +", cex = 2)

text(m.x-.7, m.y-.7, "- x -", cex = 2)

text(m.x+.7, m.y-.7, "+ x -", cex = 2)

text(m.x-.7, m.y+.7, "- x +", cex = 2)

\[(x_i - \bar{x})(y_i - \bar{y})\]

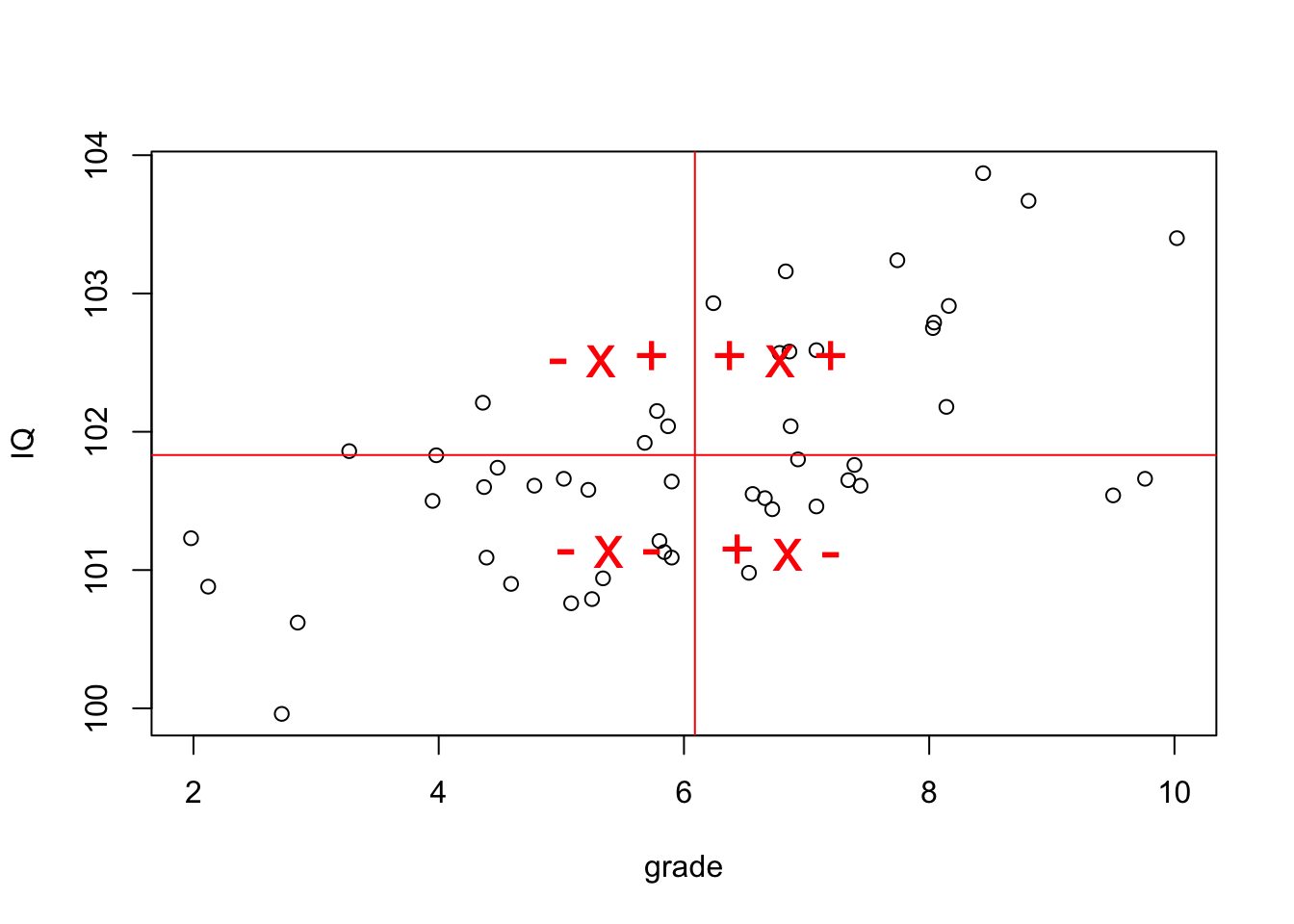

Guess the correlation

Simulate data

n = 50

grade = rnorm(n, 6, 1.6)

b.0 = 100

b.1 = .3

error = rnorm(n, 0, 0.7)

IQ = b.0 + b.1 * grade + error

#IQ = group(IQ)

error = rnorm(n, 0, 0.7)

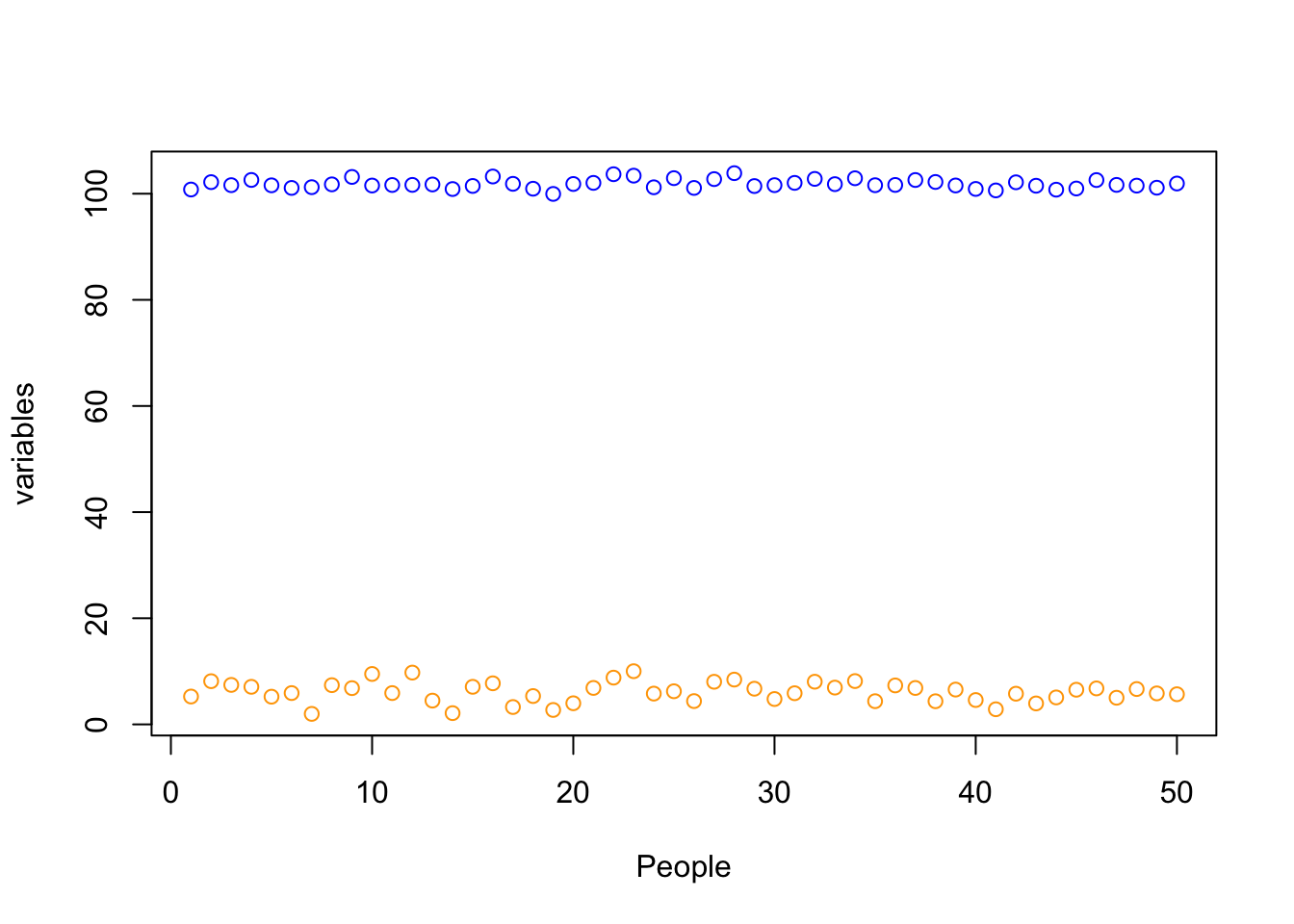

motivation = 3.2 + .2 * IQ + errorExplaining vairance

grade = data$grade

IQ = data$IQ

mean.grade = mean(grade)

mean.IQ = mean(IQ)

N = length(grade)

plot(data$grade, ylim=summary(c(data$grade, data$IQ))[c('Min.','Max.')],

col='orange',

ylab="variables",

xlab="People")

points(data$IQ, col='blue')

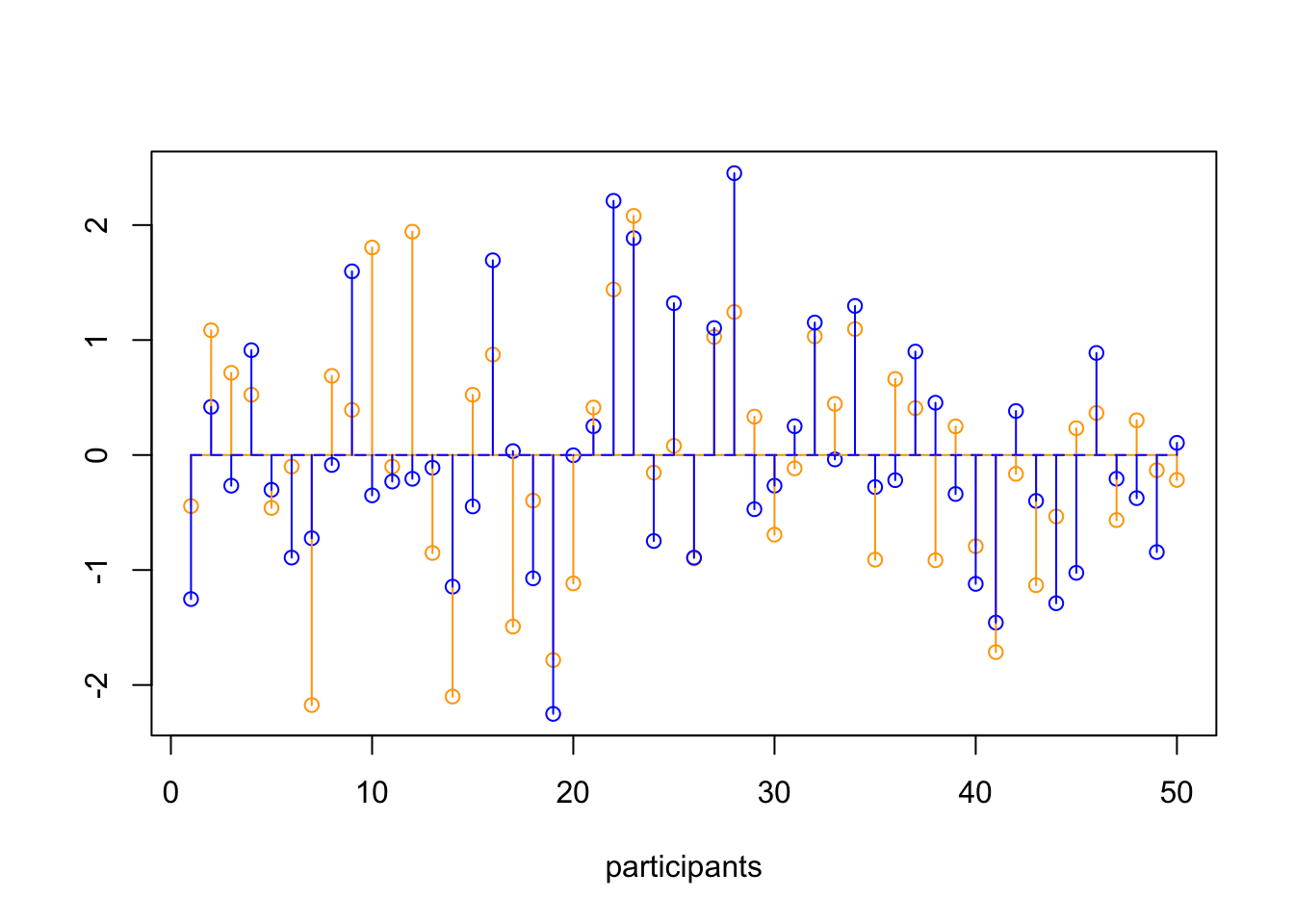

Standarize

\[z = \frac{x_i - \bar{x}}{{sd}_x}\]

data[, c('z.grade', 'z.IQ')] = scale(data[, c('grade', 'IQ')])

z.grade = data$z.grade

z.IQ = data$z.IQ

mean.z.grade = mean(z.grade, na.rm=T)

mean.z.IQ = mean(z.IQ, na.rm=T)

plot(z.grade,

ylim = summary(c(z.grade, z.IQ))[c('Min.','Max.')],

col = 'orange',

ylab = "", xlab="participants")

points(z.IQ, col='blue')

# Add mean lines

lines(rep(mean.z.grade, N), col='orange')

lines(rep(mean.z.IQ, N), col='blue', lt=2)

# Add vertical variance lines

segments(1:N, mean.z.grade, 1:N, z.grade, col='orange')

segments(1:N, mean.z.IQ, 1:N, z.IQ, col='blue')

Covariance

\[{COV}_{xy} = \frac{\sum_{i=1}^N (x_i - \bar{x})(y_i - \bar{y})}{N-1}\]

mean.grade = mean(grade, na.rm=T)

mean.IQ = mean(IQ, na.rm=T)

delta.grade = grade - mean.grade

delta.IQ = IQ - mean.IQ

prod = (grade - mean.grade) * (IQ - mean.IQ)

covariance = sum(prod) / (N - 1)Correlation

\[r_{xy} = \frac{{COV}_{xy}}{S_xS_y}\]

correlation = covariance / ( sd(grade) * sd(IQ) ); correlation[1] 0.6207285cor(z.grade, z.IQ)[1] 0.6207285cor( grade, IQ)[1] 0.6207285sum( z.grade * z.IQ ) / (N - 1)[1] 0.6207285x = c(1,-1,-1, 0,.5,-.5)

y = c(1,-1, 1, 1, 1, 1)

cbind(x,y,x*y) x y

[1,] 1.0 1 1.0

[2,] -1.0 -1 1.0

[3,] -1.0 1 -1.0

[4,] 0.0 1 0.0

[5,] 0.5 1 0.5

[6,] -0.5 1 -0.5Plot correlation

Significance of a correlation

\[t_r = \frac{r \sqrt{N-2}}{\sqrt{1 - r^2}} \\ {df} = N - 2\]

$$

\[\begin{aligned} H_0 &: t_r = 0 \\ H_A &: t_r \neq 0 \\ H_A &: t_r > 0 \\ H_A &: t_r < 0 \\ \end{aligned}\]$$

r to t

df = N-2

t.r = ( correlation*sqrt(df) ) / sqrt(1-correlation^2)

cbind(t.r, df) t.r df

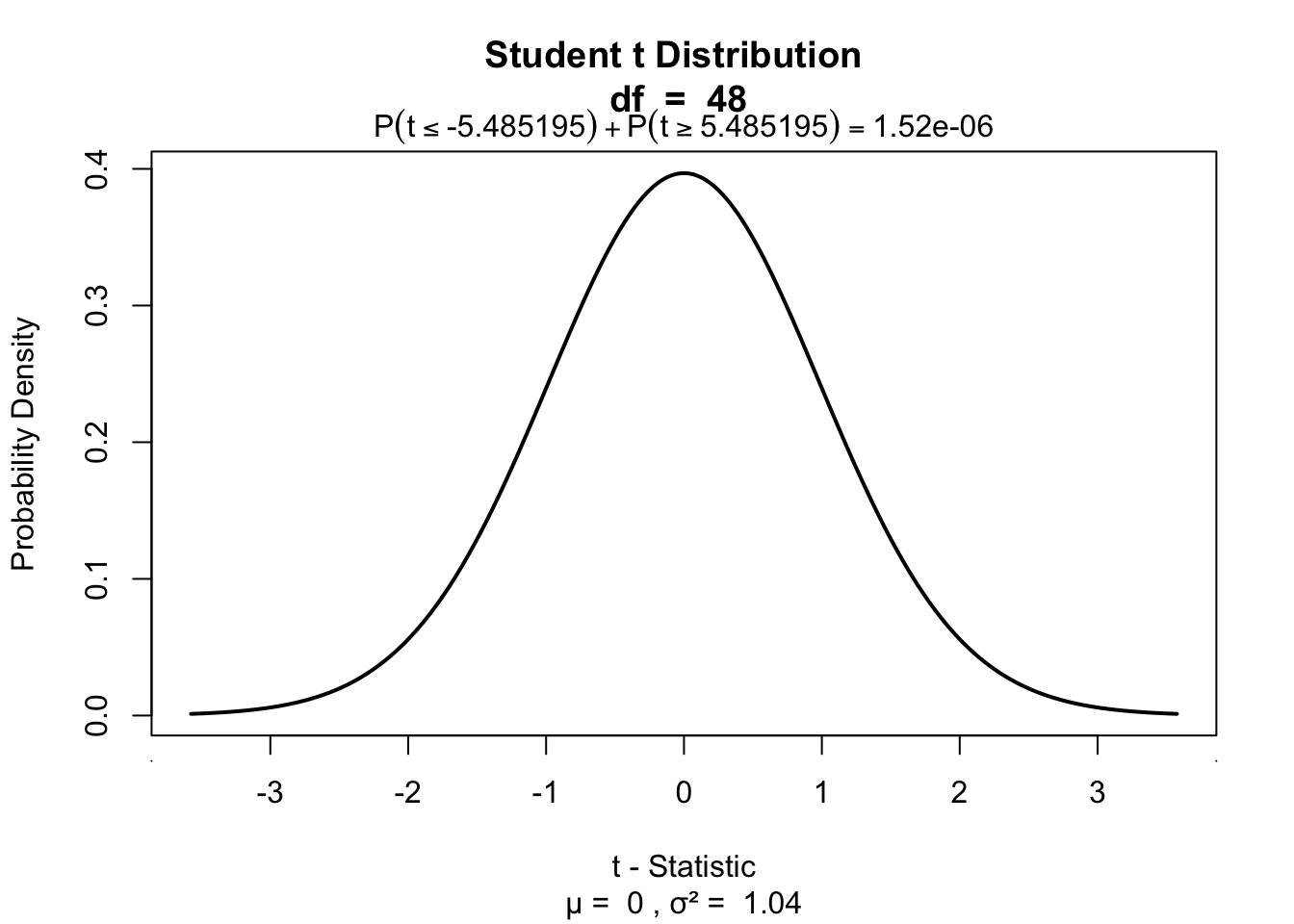

[1,] 5.485195 48Visualize

One-sample t-test

if(!"visualize" %in% installed.packages()) { install.packages("visualize") }

library("visualize")

visualize.t(c(-t.r, t.r),df,section='tails')

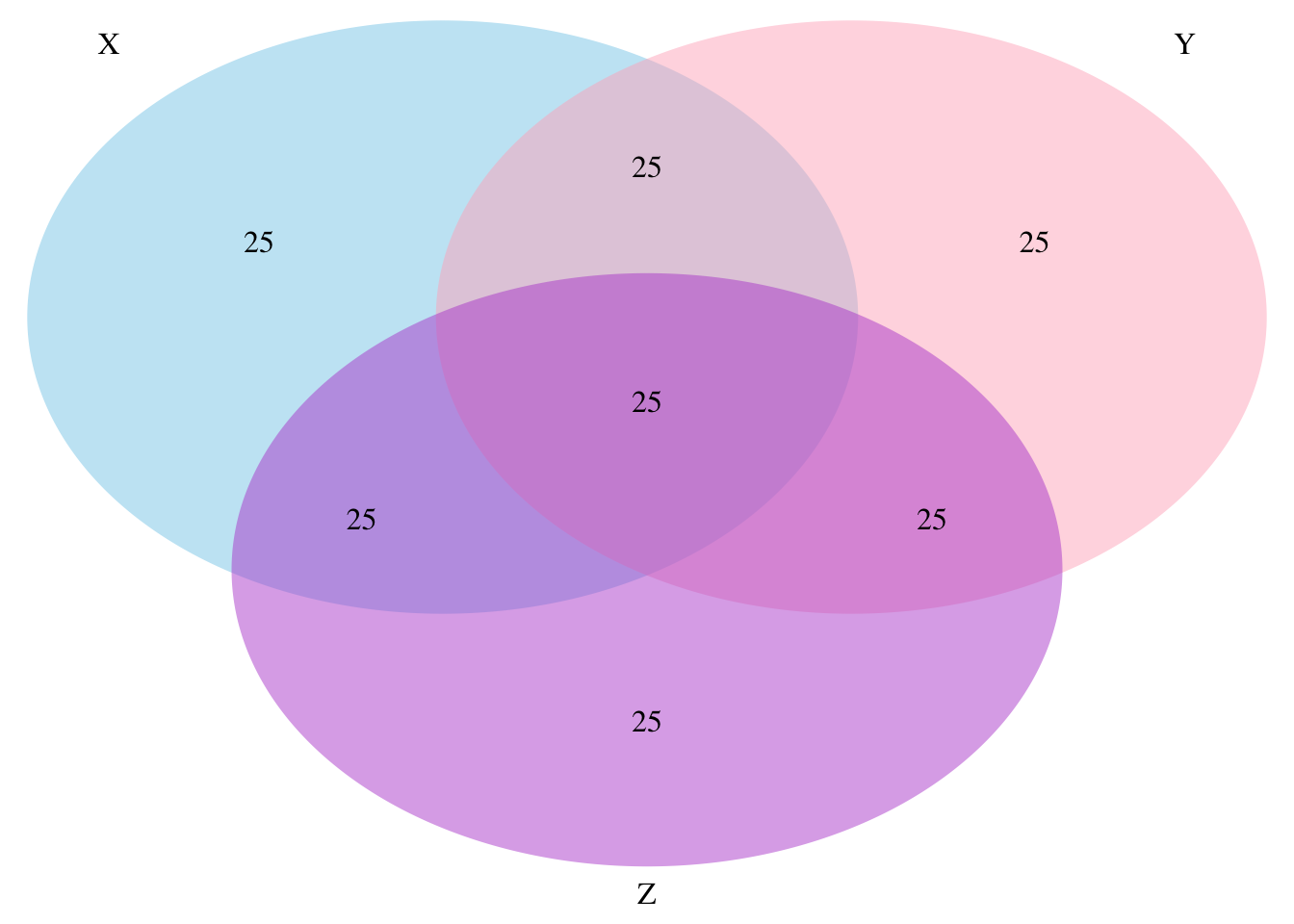

Partial correlation

Venn diagram

Partial correlation

\[\LARGE{r_{xy \cdot z} = \frac{r_{xy} - r_{xz} r_{yz}}{\sqrt{(1 - r_{xz}^2)(1 - r_{yz}^2)}}}\]

motivation = data$motivation

cor.grade.IQ = cor(grade,IQ)

cor.grade.motivation = cor(grade,motivation)

cor.IQ.motivation = cor(IQ,motivation)

data.frame(cor.grade.IQ, cor.grade.motivation, cor.IQ.motivation) cor.grade.IQ cor.grade.motivation cor.IQ.motivation

1 0.6207285 -0.1100721 0.2311468numerator = cor.grade.IQ - (cor.grade.motivation * cor.IQ.motivation)

denominator = sqrt( (1-cor.grade.motivation^2)*(1-cor.IQ.motivation^2) )

partial.correlation = numerator / denominator

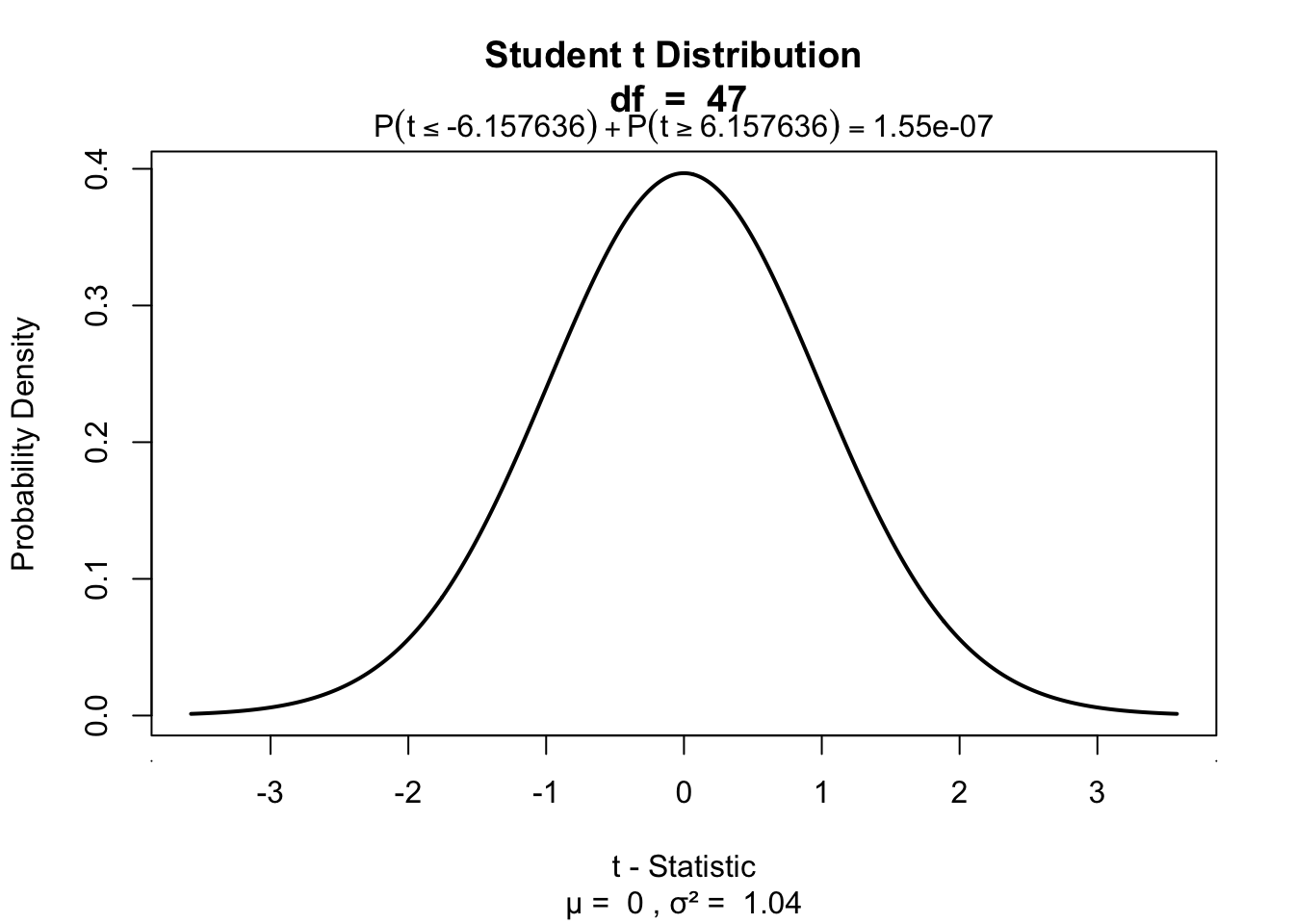

partial.correlation[1] 0.6682178Significance of parial correlation

One-sample t-test

df = N - 3

t.pr = ( partial.correlation*sqrt(df) ) / sqrt(1-partial.correlation^2)

t.pr[1] 6.157636visualize.t(c(-t.pr,t.pr),df,section='tails')

Regression

(one predictor)

Regression

\[\LARGE{\text{outcome} = \text{model} + \text{error}}\]

In statistics, linear regression is a linear approach for modeling the relationship between a scalar dependent variable y and one or more explanatory variables denoted X. The case of one explanatory variable is called simple linear regression.

\[\LARGE{Y_i = \beta_0 + \beta_1 X_i + \epsilon_i}\]

In linear regression, the relationships are modeled using linear predictor functions whose unknown model parameters are estimated from the data.

Source: wikipedia

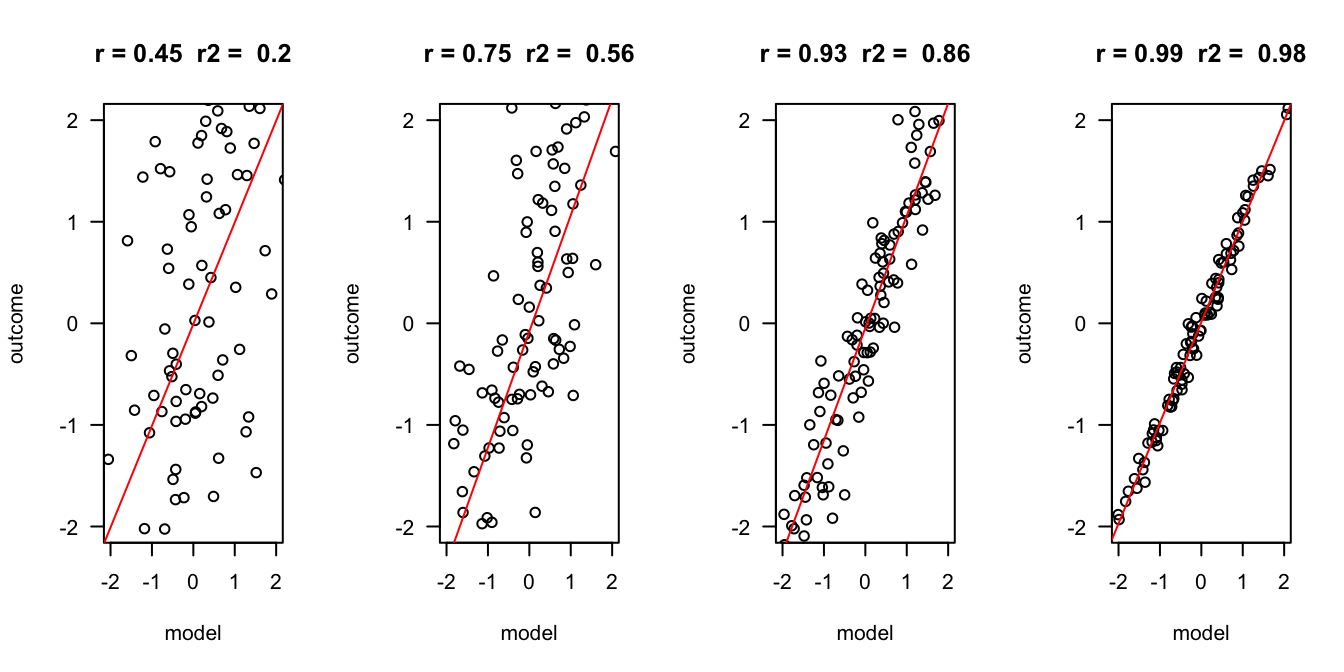

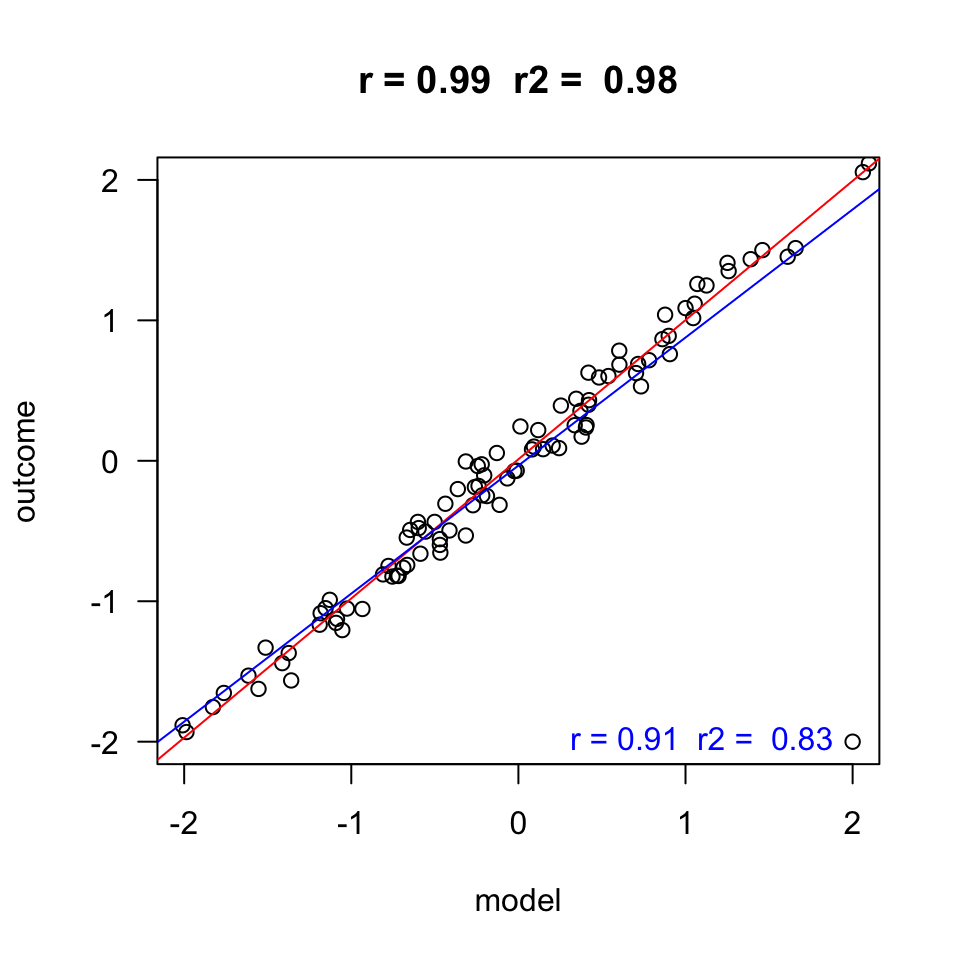

Outcome vs Model

error = c(2, 1, .5, .1)

n = 100

layout(matrix(1:4,1,4))

for(e in error) {

x = rnorm(n)

y = x + rnorm(n, 0 , e)

r = round(cor(x,y), 2)

r.2 = round(r^2, 2)

plot(x,y, las = 1, ylab = "outcome", xlab = "model", main = paste("r =", r," r2 = ", r.2), ylim=c(-2,2), xlim=c(-2,2))

fit <- lm(y ~ x)

abline(fit, col = "red")

}

Assumptions

A selection from Field:

- Sensitivity

- Homoscedasticity

Sensitivity

Outliers

- Extreme residuals

- Cook’s distance (< 1)

- Mahalonobis (< 11 at N = 30)

- Laverage (The average leverage value is defined as (k + 1)/n)

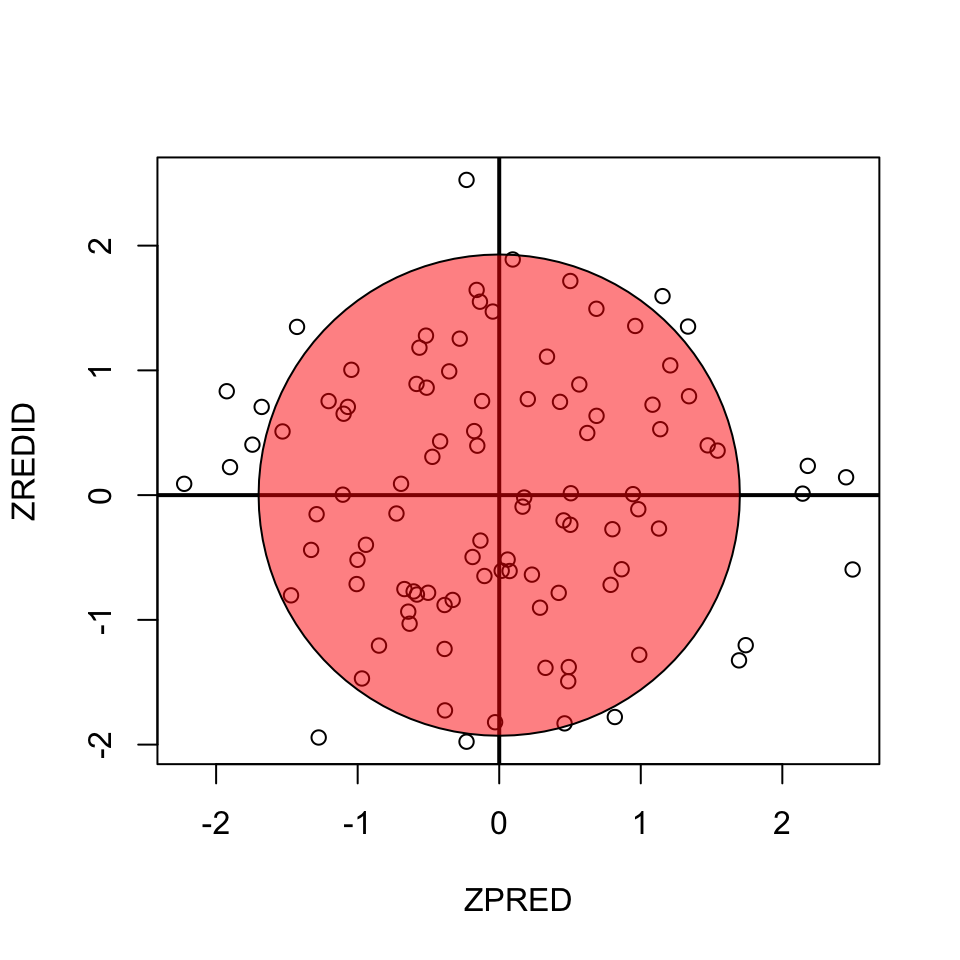

Homoscedasticity

- Variance of residual should be equal across all expected values

- Look at scatterplot of standardized: expected values \(\times\) residuals. Roughly round shape is needed.

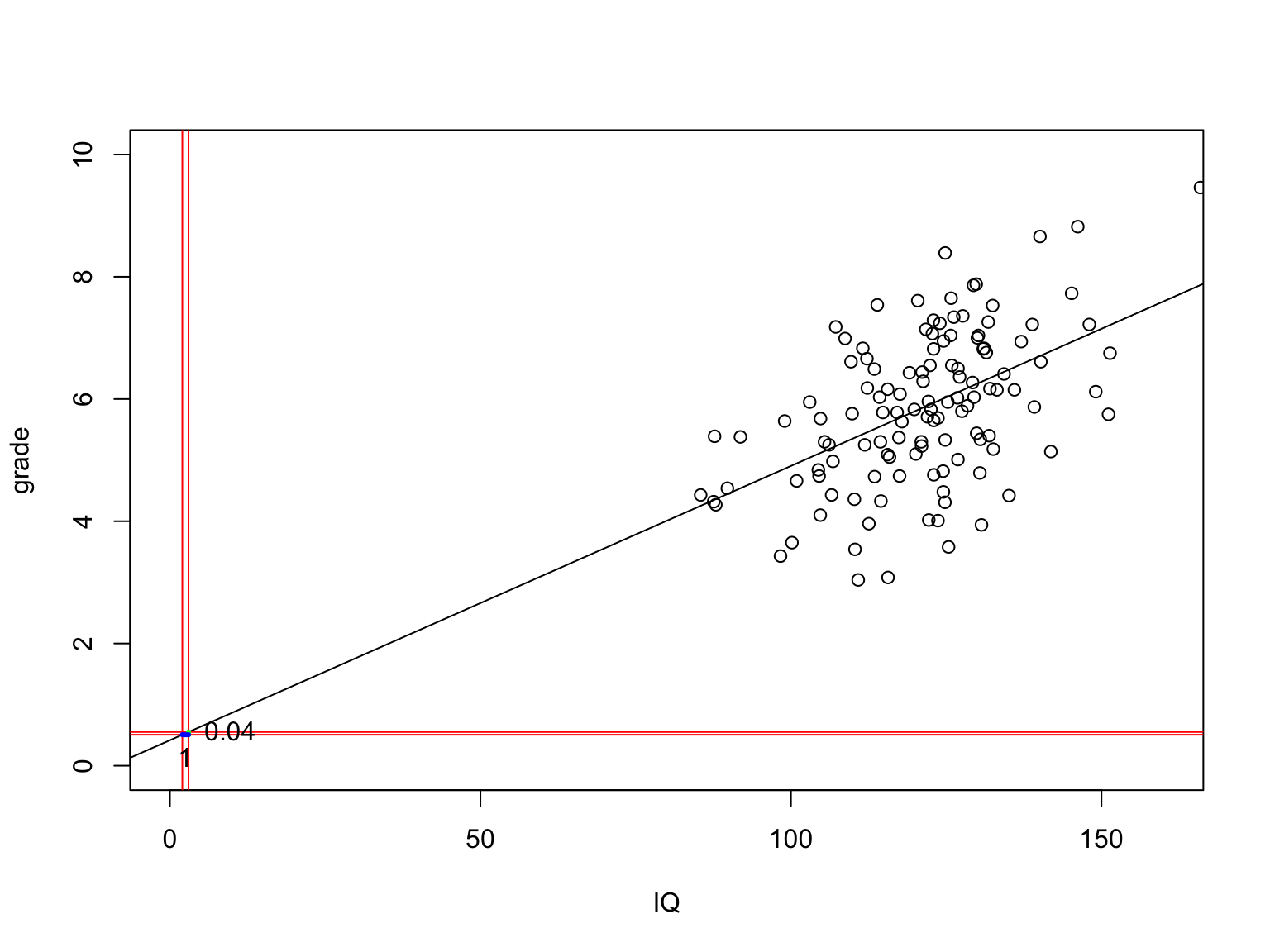

Simulation

set.seed(28736)

N = 123

mu = 120

sigma = 15

IQ = rnorm(N, mu, sigma)

b_0 = 1

b_1 = .04

error = rnorm(N, 0, 1)

grade = b_0 + b_1 * IQ + error

data = data.frame(grade, IQ)

data = round(data, 2)

# Write data for use in SPSS

write.table(data, "IQ.csv", row.names=FALSE, col.names=TRUE, dec='.')The data

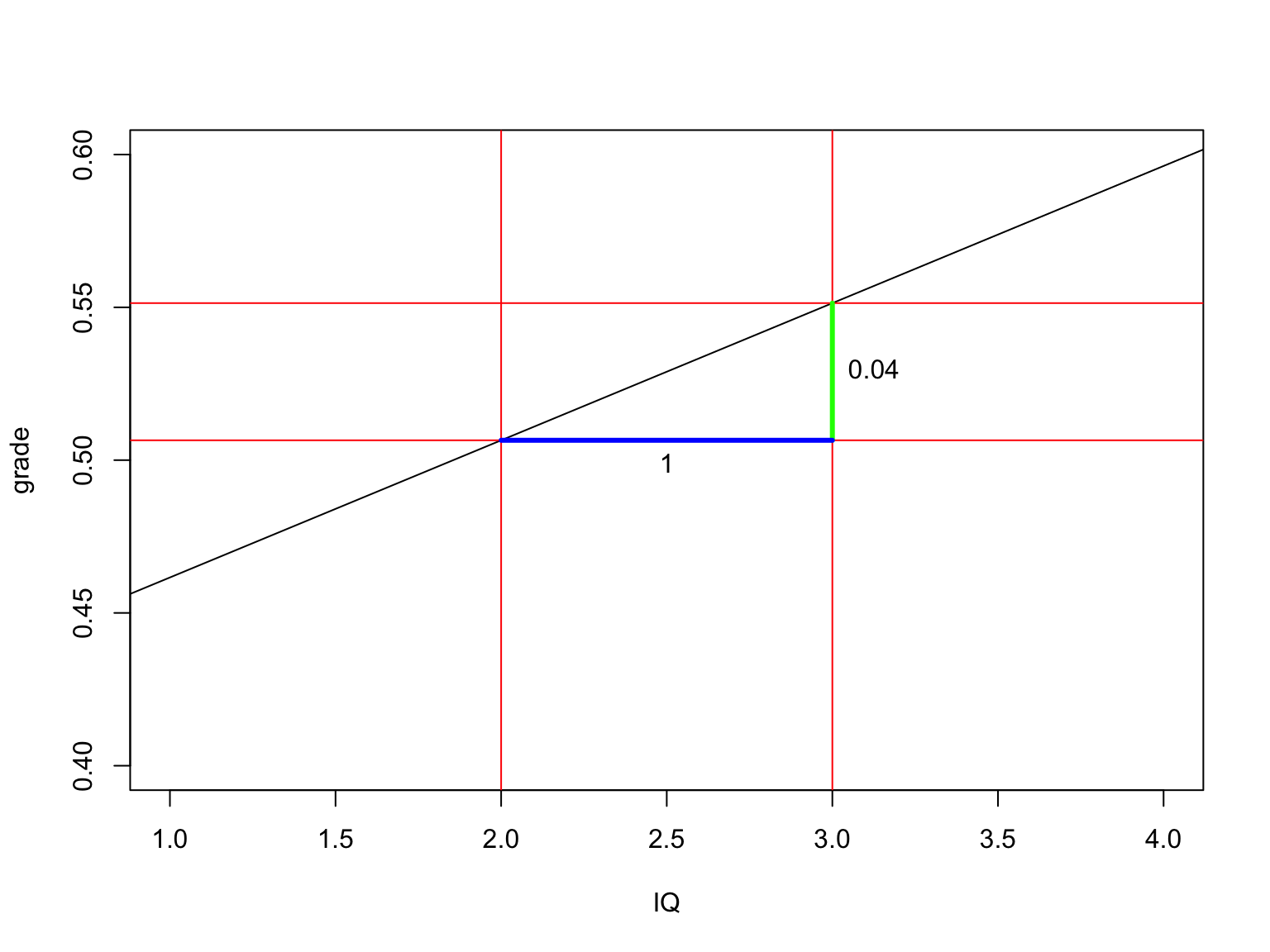

Calculate regression parameters

\[{grade}_i = b_0 + b_1 {IQ}_i + \epsilon_i\]

IQ = data$IQ

grade = data$gradeCalculate \(b_1\)

\[b_1 = r_{xy} \frac{s_y}{s_x}\]

# Calculate b1

cor.grade.IQ = cor(grade,IQ)

sd.grade = sd(grade)

sd.IQ = sd(IQ)

b1 = cor.grade.IQ * ( sd.grade / sd.IQ )

b1[1] 0.04489104Calculate \(b_0\)

\[b_0 = \bar{y} - b_1 \bar{x}\]

mean.grade = mean(grade)

mean.IQ = mean(IQ)

b0 = mean.grade - b1 * mean.IQ

b0[1] 0.4167131The slope

Calculate t-values for b’s

\[t_{n-p-1} = \frac{b - \mu_b}{{SE}_b}\]

Where \(n\) is the number of rows, \(p\) is the number of predictors, \(b\) is the beta coefficient and \({SE}_b\) its standard error.

# Get Standard error's for b

fit <- lm(grade~IQ)

se = summary(fit)[4]$coefficients[,2]

se.b0 = se[1]

se.b1 = se[2]

cbind(se.b0, se.b1) se.b0 se.b1

(Intercept) 0.8542378 0.006998539# Calculate t's

mu.b0 = 0

mu.b1 = 0

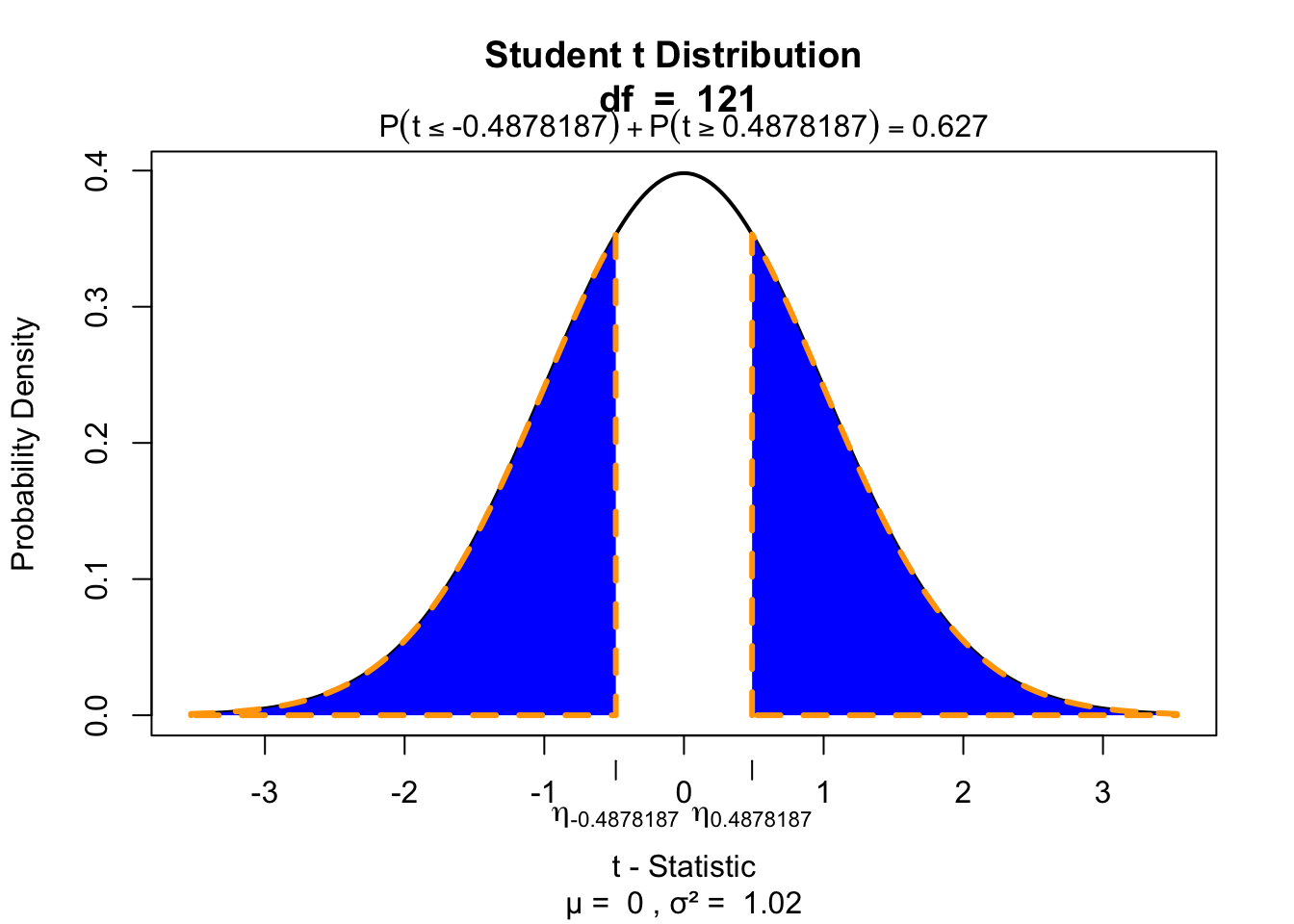

t.b0 = (b0 - mu.b0) / se.b0; t.b0(Intercept)

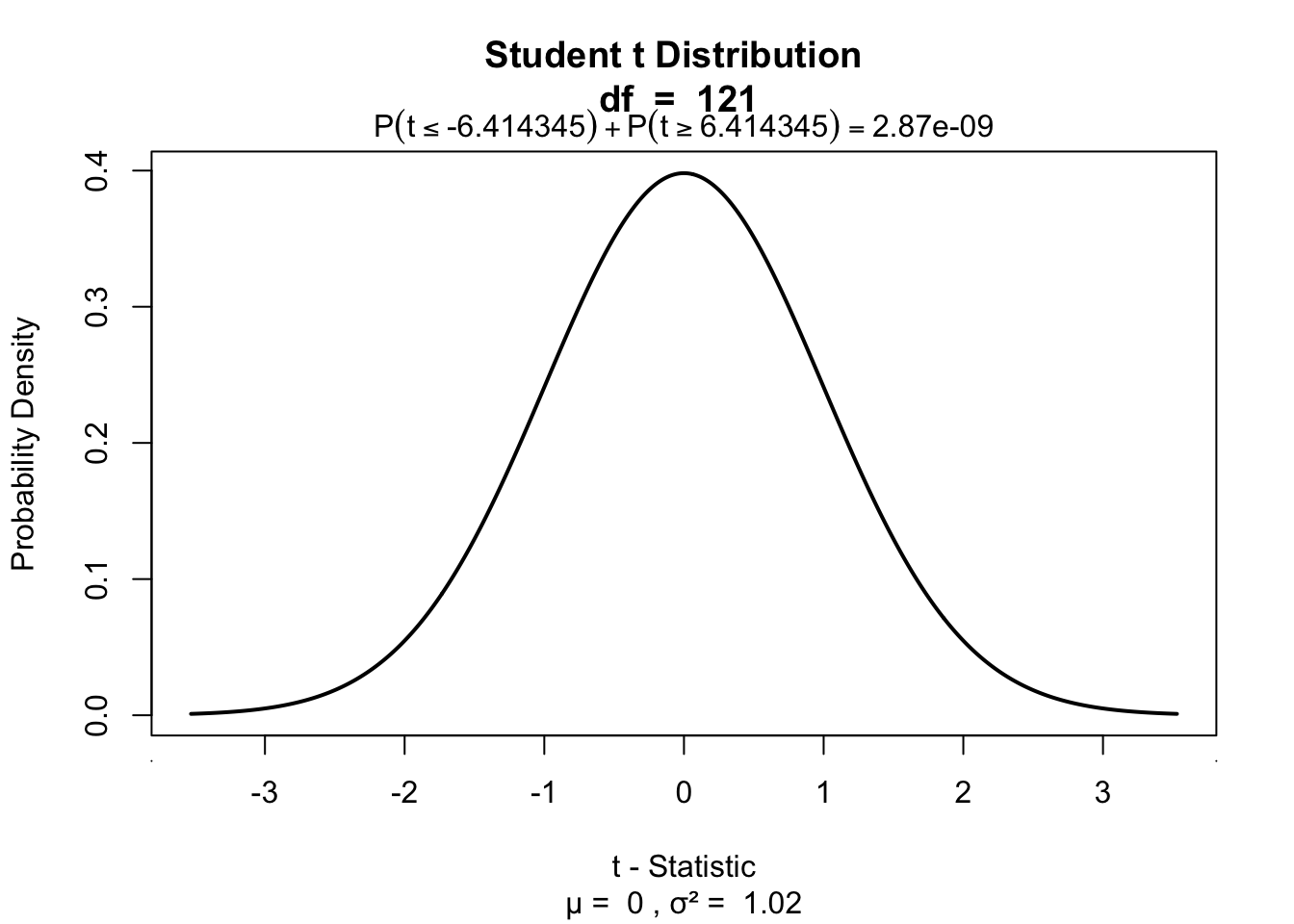

0.4878187 t.b1 = (b1 - mu.b1) / se.b1; t.b1 IQ

6.414345 n = nrow(data) # number of rows

p = 1 # number of predictors

df.b0 = n - p - 1

df.b1 = n - p - 1P-values of \(b_0\)

$$ \[\begin{aligned} t_{n-p-1} &= \frac{b - \mu_b}{{SE}_b} \\ df &= n - p - 1 \\ \end{aligned}\]$$

Where \(b\) is het beta coeficient \({SE}\) is the standard error of the beta coefficient, \(n\) is the number of subjects and \(p\) the number of predictors.

if (!"visualize" %in% installed.packages()) {

install.packages("visualize")}

library("visualize")

# p-value for b0

visualize.t(c(-t.b0,t.b0),df.b0,section='tails')

P-values of \(b_1\)

# p-value for b1

visualize.t(c(-t.b1,t.b1),df.b1,section='tails')

Define regression equation

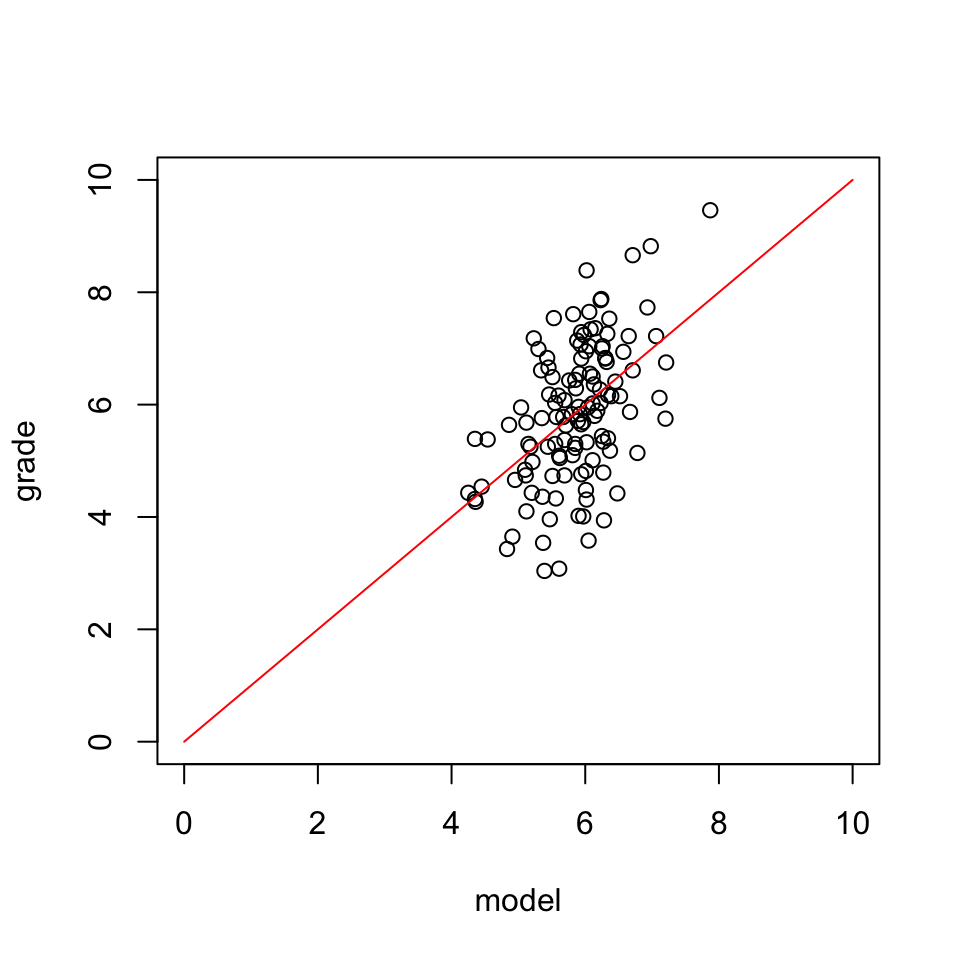

\[\widehat{grade} = {model} = b_0 + b_1 {IQ}\]

So now we can add the expected grade based on this model

data$model = b0 + b1 * IQ

data$model <- round(data$model, 2)Expected values

Let’s have a look

\(y\) vs \(\hat{y}\)

And lets have a look at this relation between expectation and reality

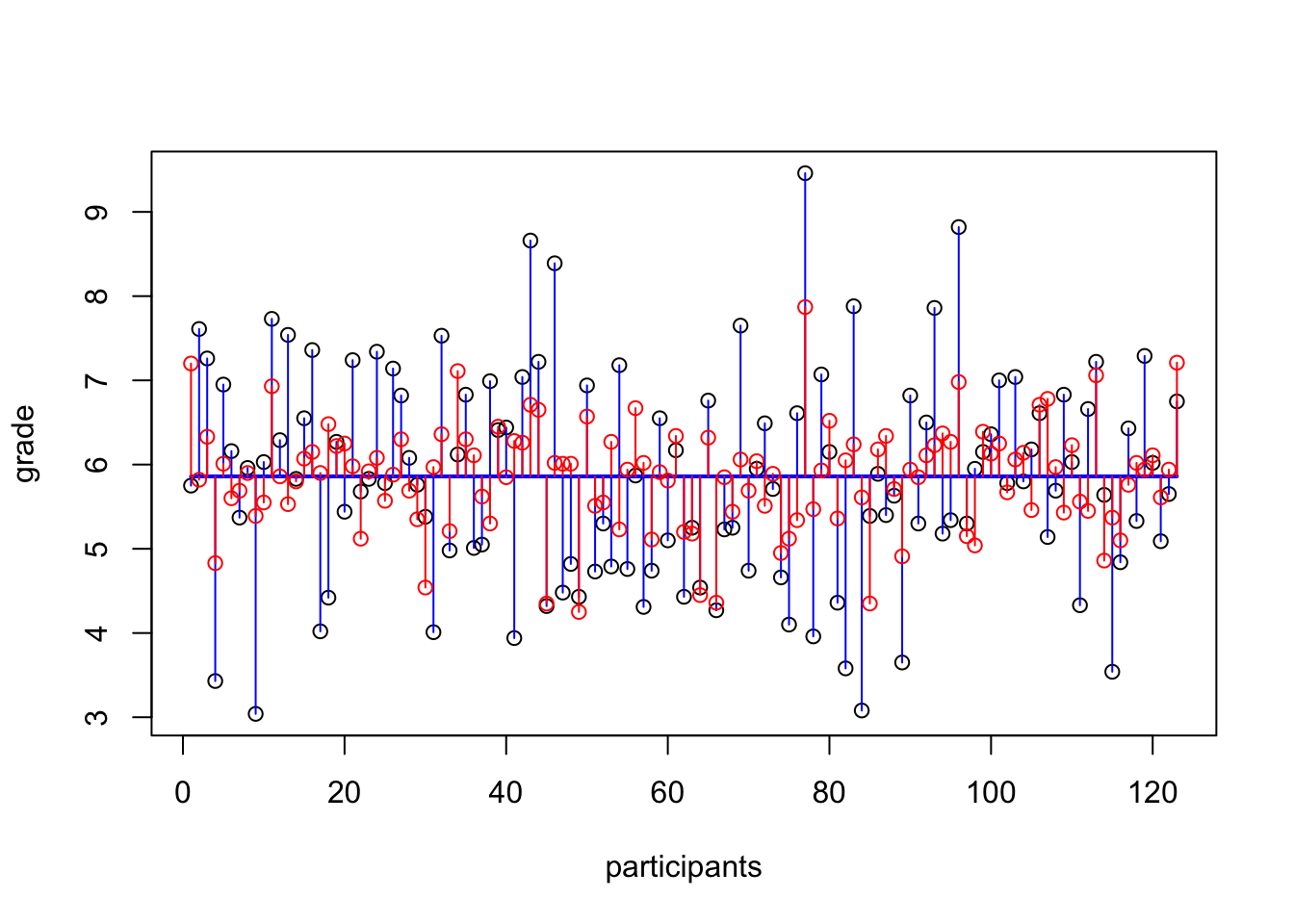

Error

The error / residual is the difference between the model expectation and reality

data$error = grade - model

data$error <- round(data$error, 2)Model fit

The fit of the model is the amount of error, which can be viewed in the correlation (\(r\)).

r = cor(model,grade)

r[1] 0.5035925Explained variance

r^2[1] 0.2536054Explained variance visually

The part that does not overlap is therefore ‘unexplained’ variance. And because \(r^2\) is the explained variance, \(1 - r^2\) is the unexplained variance.

Test model fit

Compare model to mean Y (grade) as model

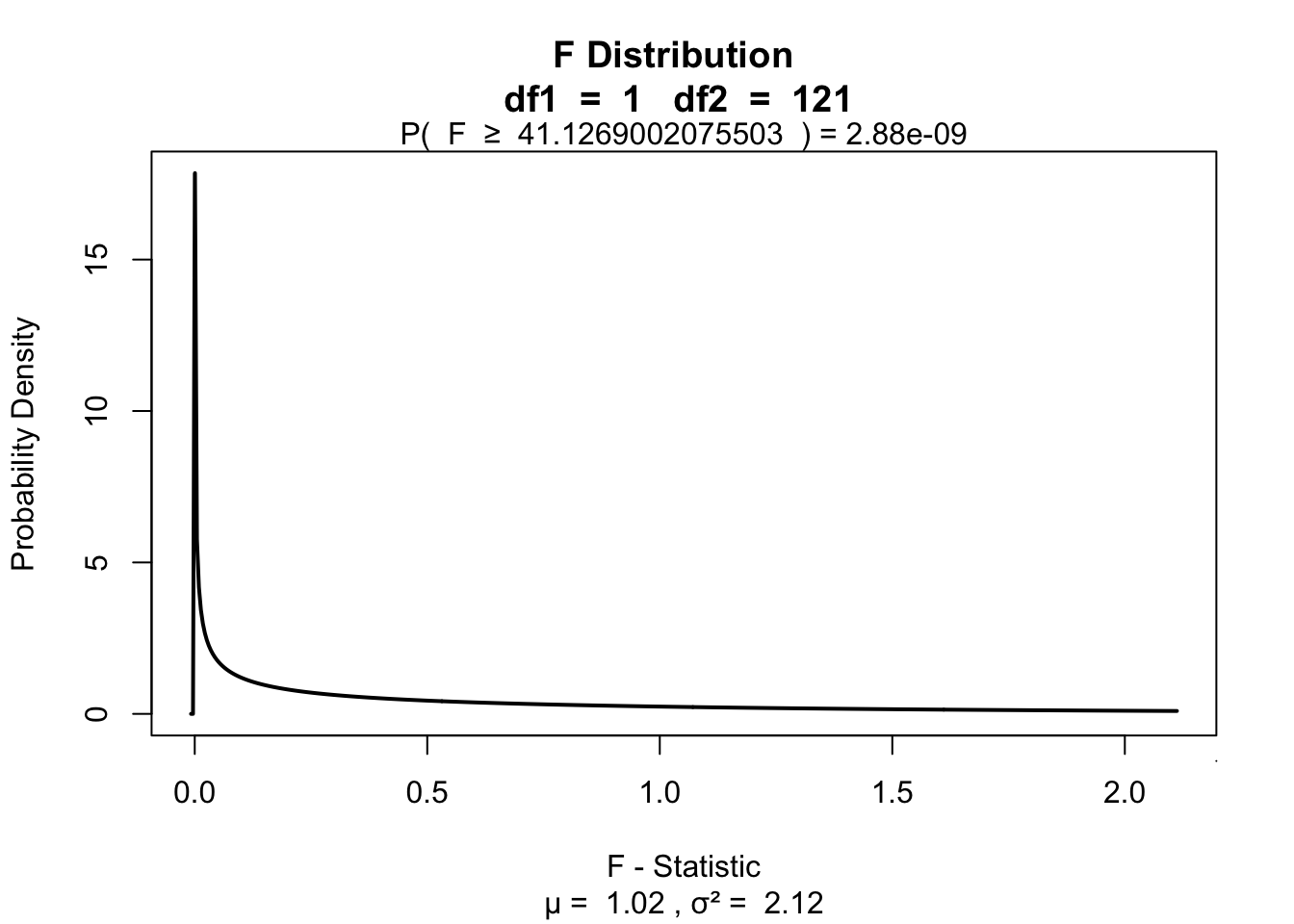

\[F = \frac{(n-p-1) r^2}{p (1-r^2)}\]

Where \({df}_{model} = n - p - 1 = N - K - 1\).

F = ( (n-p-1)*r^2 ) / ( p*(1-r^2) )

F[1] 41.11265Signal to noise

Given the description of explained variance, F can again be seen as a proportion of explained to unexplained variance. Also known as a signal to noise ratio.

df.model = p # n = rows, p = predictors

df.error = n-p-1

SS_model = sum((model - mean(grade))^2)

SS_error = sum((grade - model)^2)

MS_model = SS_model / df.model

MS_error = SS_error / df.error

F = MS_model / MS_error

F[1] 41.1269SS_total = var(grade) * (n-1)

rbind(SS_total,

SS_model,

# Proportion explained variance

SS_model / SS_total,

r^2) [,1]

SS_total 191.0732000

SS_model 48.4740000

0.2536933

0.2536054Visualize

visualize.f(F, df.model, df.error, section='upper')

End

Contact